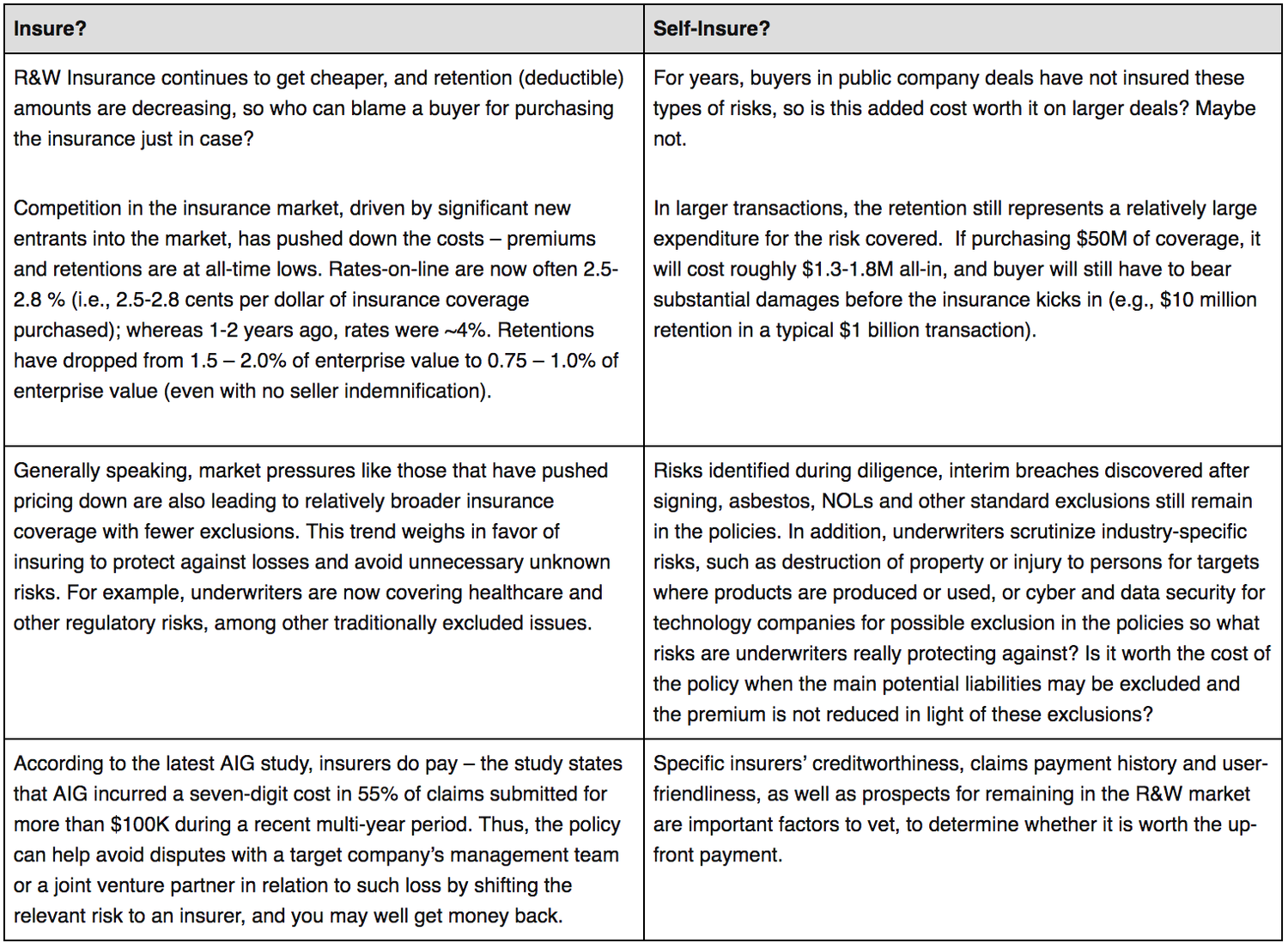

In today’s competitive, seller-friendly M&A environment, buyers are often left with the choice to insure using representation and warranty insurance or to self-insure by accepting all post-closing risk. The days of sellers standing behind their representations and warranties in the purchase agreement appear to be trending away. This note highlights several considerations for a buyer facing this decision as it looks to optimize the path forward.

For many, clearly the answer to these issues must be to insure, since statistics prove this out. There are now more than 20 R&W insurers in the US and, according to market data, more than 1,400 policies were placed in 2017, representing tens of billions of dollars in coverage limits and roughly $1 billion in premiums. Nevertheless, repeat buyers such as private equity sponsors may question the value of obtaining R&W insurance in a particular transaction, particularly if they have done so frequently in past transactions but have not submitted (or received payment for) many claims. The initial outlay of premium and costs required to procure the insurance, coupled with the retention and potential exclusions may cause buyers (particularly those with large, diversified acquisition portfolios) to prefer to retain the risk of losses resulting from seller rep breaches by self-insuring. An obvious risk of self-insuring is an unexpected, catastrophic loss that materially diminishes the value of the buyer’s investment – the type of loss that R&W insurance is essentially designed to cover. Ultimately, the question devolves into a commercial, risk-tolerance and cost-benefit-analysis that each buyer must perform on a case-by case basis.

To see the original article, please click here.

This article was written by Gabriel Gershowitz and Brian Gingold and was published by Weil Gotshal & Manges, LLP.